First-Time Buyer Rent-vs-Buy in Anaheim (2026): Can Your Budget Make the Payment Jump?

Quick Answer

Your first real question is whether your budget can carry a full ownership payment: principal and interest, plus property tax, insurance, any HOA, and mortgage insurance if it applies, compared with the rent check you write now. The financing path you pick moves that monthly number, your down payment, and whether mortgage insurance shows up at all. FHA, conventional, and other loan types differ on down payment, mortgage insurance, and credit flexibility5; the right one depends on your savings, credit, and how long you plan to stay. Budget the ongoing carry and the cash-to-close, then get pre-approved with a licensed mortgage loan originator.

Anaheim first-time buyer at a glance

| Median sale price | $948,000 |

| Days on market | 34 days |

| 30-year fixed rate | 6.49% |

| Orange County conforming loan limit | $1,249,125 |

Sourced figures (see Sources & Data). Payment and tax estimates below are illustrative; confirm yours with a lender.

The defining pressure for a first-time buyer in Anaheim is the leap from a rent check to a full ownership payment: principal and interest, property tax, insurance, and any HOA or mortgage insurance, and whether your budget actually carries the total. The loan you choose drives that monthly figure more than most people expect. Here’s the thing about staying conforming: it hinges on your loan amount, not the sticker price. With an Anaheim median around $948,0001, many purchases fall under the Orange County conforming loan limit of $1,249,1253, which keeps conventional financing accessible, but your loan amount, not the price, determines whether a loan is conforming or jumbo. We’ll build everything around that rent-versus-own reality, then work through FHA vs conventional, the cost of ownership, the cash to close, and offer a strategy.

Anaheim Buyer Snapshot

Start with where the numbers sit right now. The current Redfin median sale price in Anaheim is $948,0001, with homes selling in a median of 34 days1. Financing costs matter just as much as price. As of July 9, 2026, the 30-year fixed rate is 6.49%, and the 15-year fixed is 5.82%2; rates change weekly, so lock timing matters.

🏠 Anaheim Buyer Context

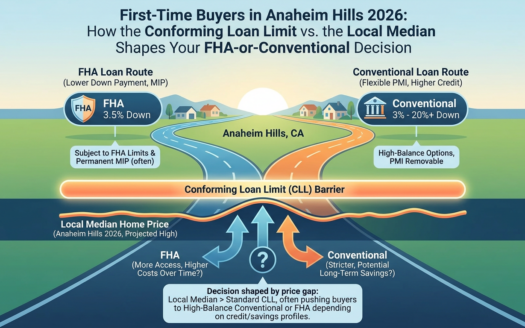

FHA vs. Conventional: Which Path Fits

You’ll most likely weigh two paths: FHA and conventional. FHA can open the door with a smaller down payment and more flexibility on credit, but it carries its own mortgage insurance structure. Conventional loans often require more down payment and stronger credit, yet they can drop mortgage insurance once you build enough equity. Each path shifts your down payment, your monthly cost, and your qualifying picture, so the table below lays the trade-offs side by side.

| Consideration | FHA | Conventional |

|---|---|---|

| Down payment | Lower entry point | Often higher, with more flexibility |

| Mortgage insurance | Required; stays for most loans | Can be removed once you build equity |

| Credit flexibility | More forgiving | Rewards stronger credit |

| Best fit | Lower savings/building credit | Stronger savings / longer hold |

A licensed mortgage loan originator can model both for your numbers; this table is a planning framework, not a recommendation.

- Lean FHA: when your down payment savings are limited or your credit is still building, you accept mortgage insurance for a lower entry point.

- Lean conventional, when you have stronger savings and credit, and want the option to drop mortgage insurance as you build equity.

- Either way, have a lender model the real monthly payment and total cash-to-close on both before you choose; the lower down payment is not always the cheaper loan over the years you hold it.

FHA can help some Anaheim buyers, but not every purchase here will fit FHA loan limits or property requirements. The conforming loan limit above applies to conventional conforming loans; FHA uses separate county loan limits. Ask your lender to confirm the current Orange County FHA loan limit, the required down payment, mortgage insurance, and property eligibility before assuming FHA is available for a specific home.

One distinction trips up a lot of buyers: the conforming loan limit applies to conventional conforming loans, and FHA runs on a separate set of county loan limits entirely. If you’re leaning toward an FHA loan, confirm the current Orange County FHA loan limit with your lender rather than assuming the conventional figure applies. And if a home sits just above your applicable limit, a larger down payment can shrink the loan enough to keep the purchase conforming. Small changes to your cash can change which product you qualify for.

What a First-Time Buyer in Anaheim Pays Each Month

Turn those figures into planning math so you can see the payment before you fall for a house. As an illustration, financing the $948,000 median1 with 20% down at the 6.49% 30-year rate2 puts the principal-and-interest portion alone near $4,789 a month; a smaller down payment raises both the loan and the monthly cost and usually adds mortgage insurance, property taxes, homeowners insurance, and any HOA fees, so confirm your real number with a licensed mortgage loan originator. Your down payment size and any mortgage insurance are the two levers that move the base figure the most. Treat it as a starting frame, not a quote.

The Real Cost of Owning, Beyond Principal and Interest

Owning costs more each month than the loan payment itself, and the extras add up quietly. Beyond principal and interest, plan for the ongoing cost of ownership: at California’s 1% Prop 13 base rate7, a $948,000 home1 runs about $9,480 a year in base property tax before local voter-approved bonds and any Mello-Roos assessments, plus homeowners insurance and any HOA dues. Some Anaheim properties may carry Mello-Roos or other special assessments while others may not, so don’t assume based on a neighborhood’s name, age, or location. On any specific home, confirm the actual property tax bill, parcel-specific assessments, HOA dues, and a real insurance quote before you write an offer.

- Property taxes, near California’s Prop 13 base rate, plus local voter-approved bonds, and possible Mello-Roos or special assessments, depending on the parcel.

- Homeowners insurance, which can cost more where a parcel sits in a mapped fire zone.

- Mortgage insurance, on most low-down-payment loans until you reach enough equity, though FHA often keeps it for the life of the loan.

- HOA dues, common across many Anaheim communities.

- Maintenance and repairs, the costs a first home adds that renting never did.

Cash to Close: More Than the Down Payment

The down payment is only one line in the cash you’ll bring to closing. Your cash to close is more than the down payment: it also includes closing costs like lender fees, title, escrow, appraisal, and recording, plus prepaid property taxes and homeowners insurance; federal rules require your lender to give you a Loan Estimate that itemizes your closing costs and total cash to close within three business days of your application4, so ask for one early. Reserves that the lender wants you to keep on hand can push the number higher still. Reading that Loan Estimate line by line is how you avoid a surprise the week before you sign.

- Closing costs, lender fees, title, escrow, appraisal, and recording.

- Prepaid items, property taxes, and homeowners’ insurance are collected up front.

- Reserves, some loans require you to keep a few months of payments in the bank (verified, not paid at closing).

- Earnest money, your good-faith deposit, is credited toward your costs at closing.

- Inspections are paid out of pocket during escrow.

Your lender’s Loan Estimate itemizes these. Ask for one before you commit to a home.

Writing a Competitive First Offer in Anaheim

Writing a competitive offer as a first-time buyer in Anaheim starts with reading the pace. Recent Anaheim sales have closed near 100.77% of list price, with 49.2% of homes selling above asking1, so a clean, fully documented pre-approval and a realistic offer can matter as much as price. You can’t control what a seller wants, but you can control your file: an underwriting-backed pre-approval rather than a basic prequalification, verified proof of funds, realistic timelines, and a responsive licensed mortgage loan originator, with your inspection and appraisal protections kept in place. Price the offer to the comps, include earnest money, and match the seller’s priorities where you reasonably can. A seller reads a tight, fully documented offer as lower risk, and in a competitive market, that credibility can matter as much as the number.

Three Ways the Decision Tends to Play Out

Most buyers we work with land in one of a handful of situations, and the same FHA-versus-conventional math points in different directions depending on your savings, credit, target price, and how much you can put down. Find the one closest to yours below.

- Lower savings, flexible on property type: FHA may be worth modeling if the price and property qualify and you need the lower entry point, just confirm the FHA limit and mortgage insurance with your lender.

- Stronger savings and credit: conventional is often cleaner if you can keep the loan under the conforming limit and want the option to drop mortgage insurance as you build equity.

- Higher price, smaller down payment: you may need a jumbo or another structure, so lender strategy matters before you tour, and a larger down payment can sometimes keep you conforming.

Rent vs. Own: a HUD Rent Benchmark

To weigh renting against owning, set a likely housing payment next to a published rent benchmark. HUD’s FY2026 Fair Market Rent for the Santa Ana-Anaheim-Irvine, CA HUD Metro FMR Area is $3,236/mo for a two-bedroom and $4,393/mo for a three-bedroom unit6; HUD Fair Market Rent is a regional payment-standard benchmark, not a market quote or a guarantee of achievable rent, so use it as a conservative reference and confirm true market rent locally. Actual asking rents can vary widely by unit size, condition, location, parking, and included utilities, so treat HUD’s number only as a regional benchmark.

Set that benchmark against ownership. The illustrative principal-and-interest alone on the $948,000 median1 at the 6.49% 30-year rate2 runs near $4,789 a month before property taxes, insurance, and any HOA or mortgage insurance, so at today’s rates, a first purchase in Anaheim often carries a higher monthly cost than the HUD rent benchmark6. That gap is why the rent-versus-own decision usually turns on how long you plan to stay: the longer you hold, the more equity builds, and any appreciation can offset the higher monthly cost and the cash you spent to close, whereas a short expected stay often favors renting. These are illustrative figures, not a quote, so model your own rent-versus-own numbers with a licensed mortgage loan originator before you decide.

Your Next Steps as a First-Time Anaheim Buyer

- Get pre-approved on both paths: ask a licensed mortgage loan originator to model FHA and conventional loans side by side to compare your savings and credit.

- Separate price from loan amount: what you borrow, not the sticker price, decides conforming vs jumbo.

- Budget the full picture: the monthly payment, the taxes and insurance on top, and the cash to close are three separate numbers, run all three before you fall in love with a listing.

- Plan your offer: in a competitive market, a clean pre-approval and a tight close can matter as much as price. Reach out, and we can help you compare Anaheim price ranges, review your offer strategy, and outline next steps while your licensed mortgage loan originator models the financing.

Frequently Asked Questions for First-Time Buyers in Anaheim

How do I know if I can handle the jump from renting to owning in Anaheim?

Compare your current rent with the full projected ownership payment, not just principal and interest. Include property taxes, homeowners’ insurance, HOA dues, mortgage insurance, maintenance, and the cash needed to close. Then have a licensed mortgage loan originator model FHA, conventional, and down-payment options so you can see the monthly payment and cash-to-close side by side, and weigh that total against the rent you pay today.

What can I realistically afford in Anaheim at today’s rates?

Affordability tracks the rate you can lock as much as the price you target. As of July 9, 2026, the 30-year fixed rate is 6.49%, and the 15-year fixed is 5.82%2; rates change weekly, so lock timing matters. Run your income, debts, and down payment through a lender’s model to see the real number, since your file, not an average, sets your ceiling.

Does Anaheim’s median price mean I need a jumbo loan?

Not necessarily. Conforming versus jumbo turns on your actual loan amount, not the purchase price. A larger down payment can shrink an above-limit purchase back into conforming territory, while a small down payment can tip a pricier home into jumbo. Confirm your specific loan amount and current limit with a licensed mortgage loan originator before you assume either.

Should a first-time buyer use an FHA or a conventional loan in Anaheim?

There’s no universal answer, and we don’t push one path for everyone. FHA, conventional, and other loan types differ on down payment, mortgage insurance, and credit flexibility5; the right one depends on your savings, credit, and how long you plan to stay. Model both with a lender using your real numbers, then compare the monthly cost and the cash required side by side.

What does it cost to own an Anaheim home beyond the mortgage payment?

Plenty. Beyond principal and interest, plan for the ongoing cost of ownership: at California’s 1% Prop 13 base rate7, a $948,000 home1 runs about $9,480 a year in base property tax before local voter-approved bonds and any Mello-Roos assessments, plus homeowners insurance and any HOA dues. Mello-Roos and other special assessments vary by parcel, so confirm the actual tax bill and assessment details for the specific property before you count on a figure.

How much cash do I need to close, beyond the down payment?

More than the down payment, the gap surprises people. Your cash to close is more than the down payment: it also includes closing costs like lender fees, title, escrow, appraisal, and recording, plus prepaid property taxes and homeowners insurance; federal rules require your lender to give you a Loan Estimate that itemizes your closing costs and total cash to close within three business days of your application4, so ask for one early. Any required reserves sit on top of that.

How competitive are offers for first-time buyers in Anaheim?

Expect to compete on terms, not just price. Recent Anaheim sales have closed near 100.77% of list price, with 49.2% of homes selling above asking1, so a clean, fully documented pre-approval and a realistic offer can matter as much as price. What you control is your file and your contingencies, so bring both in tight from the first offer, without waiving your inspection or appraisal protections without professional advice and a clear risk review.

Not Sure What Your First Anaheim Home Really Costs?

Wendy Rawley can help you compare Anaheim price ranges and the real monthly and upfront numbers, and offer a strategy while your licensed lender models FHA, conventional, and down-payment scenarios for your situation.

📞 Call (714) 746-6355🌐 Visit go2wendy.comServing Anaheim and North Orange County since 2011 | DRE #01898824

Wendy Rawley

REALTOR® | DRE #01898824

Wendy Rawley and The Wendy Rawley Team help first-time buyers in Anaheim compare neighborhoods, offer strategy, and price ranges while coordinating with the buyer’s licensed mortgage lender on financing assumptions across North Orange County.

Across North Orange County, the team has represented sellers in 114 transactions and buyers in 76, including 35 here in Anaheim8. These figures reflect prior closed transactions and do not guarantee future results.

Sources & Data

1 Redfin, Anaheim Housing Market Data

Redfin Data Center, published, downloadable market metrics (median sale price, inventory, days on market, months of supply, and year-over-year trends) by region, including Anaheim.

2 Freddie Mac, Primary Mortgage Market Survey

Weekly national average 30-year and 15-year fixed mortgage rates.

3 FHFA, Conforming Loan Limit Values

Orange County 2026 high-cost-area one-unit conforming loan limit: $1,249,125.

4 Consumer Financial Protection Bureau, What is a Loan Estimate?

Federal explainer: your lender must give you a Loan Estimate within three business days of your application; it itemizes your estimated closing costs and the total estimated cash you need to close.

5 Consumer Financial Protection Bureau, Loan Options

Federal explainer comparing conventional, FHA, VA, and USDA loan options for buyers.

6 U.S. Department of Housing and Urban Development, Fair Market Rents (FY2026)

HUD Fair Market Rents for the Santa Ana-Anaheim-Irvine, CA HUD Metro FMR Area: the payment-standard benchmark (40th-percentile gross rent) used for federal housing programs. A regional reference covering Orange County, not a market quote for Anaheim.

7 California Prop 13 / Orange County property tax

California limits the base property-tax rate to 1% of assessed value (Prop 13), plus local voter-approved bonds and any Mello-Roos. Confirm the exact tax rate, any Mello-Roos, and special assessments for a specific parcel.

8 California Regional Multiple Listing Service (CRMLS)

The Wendy Rawley Team’s closed-transaction counts (2012-2025) are drawn from CRMLS sold records, the regional multiple listing service for Southern California.

Disclaimer: This article is for informational purposes only and does not constitute legal, tax, financial, or mortgage-lending advice. Real estate commissions are negotiable and vary by brokerage. Mortgage rates, terms, and qualification criteria vary by lender and change frequently. Consult qualified professionals, including a CPA, a real estate attorney, and a licensed mortgage loan originator, regarding your specific situation. The Wendy Rawley Team | Circa Properties | DRE #01898824.

Equal Housing Opportunity.